ATAL PENSION YOJANA: NEED FOR OUTCOME-LED DEEPENING

ATAL PENSION YOJANA: NEED FOR OUTCOME-LED DEEPENING

Why in the News?

- The discussion around Atal Pension Yojana has gained attention as experts argue that the scheme must now move beyond enrolment expansion towards ensuring adequate and sustainable retirement security.

- Concerns have been raised regarding low pension adequacy, contribution persistence, and the need for greater flexibility for informal sector workers.

Achievements and significance of APY

- Social security expansion: APY has emerged as a major pension inclusion initiative targeting low-income households and unorganised sector workers.

- Rapid enrolment growth: Subscribers increased sharply from 8 lakh in 2016 to nearly 9 crore by March 2026.

- Youth participation: Nearly 70% subscribers belong to the 18–30 age group, enabling longer contribution periods and improved pension outcomes.

- Gender inclusion: Women account for nearly 5% of subscribers, highlighting growing female participation in pension savings.

- Bridge to financial inclusion: The scheme complements initiatives such as Pradhan Mantri Jan-Dhan Yojana, Direct Benefit Transfers, and the broader digital financial ecosystem.

Challenges and reforms needed

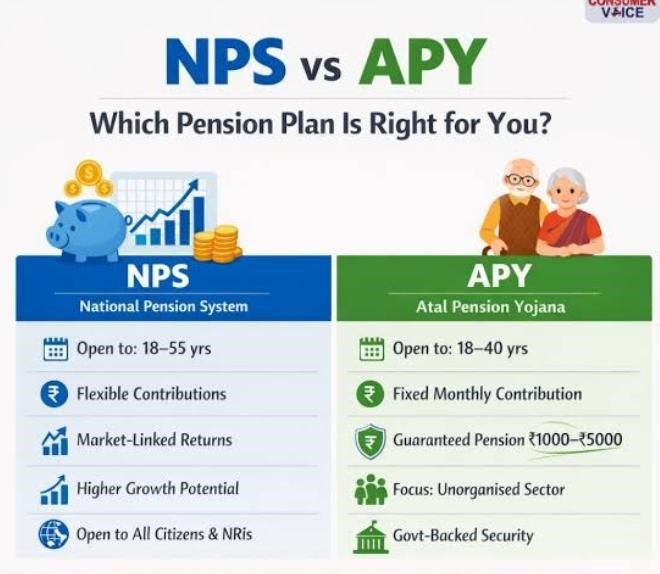

- Low pension adequacy: The guaranteed pension of ₹1,000–₹5,000 may lose relevance over time without inflation indexation or periodic revision.

- Persistency concerns: Contribution continuity remains weak, with aggregate persistency reportedly around 50%, affecting retirement security outcomes.

- Need for flexibility: Informal workers require options like temporary contribution pauses, variable payments, and pension slab upgrades linked to income cycles.

- Financial literacy gap: Limited awareness in rural and semi-urban regions reduces participation and understanding of long-term retirement planning.

- Outcome-led deepening: Experts suggest focusing on regular contributions, pension adequacy, subscriber education, and digital servicing rather than only increasing enrolment numbers.

Pension reforms in India● National Pension System (NPS): A market-linked voluntary pension scheme regulated by Pension Fund Regulatory and Development Authority. ● Employees’ Provident Fund (EPF): Provides retirement savings mainly for workers in the organised sector. ● Demographic transition: Rising life expectancy and informal employment increase the importance of sustainable pension systems. ● Financial inclusion linkage: Pension schemes are increasingly integrated with banking, digital payments, and welfare delivery systems. ● UPSC relevance: Important for GS Paper II and III under social justice, welfare schemes, financial inclusion, and inclusive economic development. |