NPS Withdrawal Rules 2026 and New Retirement Strategies

NEW NPS WITHDRAWAL RULES: GREATER FLEXIBILITY FOR RETIREMENT PLANNING

Why in the News?

- Major Reform: The Pension Fund Regulatory and Development Authority (PFRDA) has revised the National Pension System (NPS) withdrawal rules, making retirement corpus more flexible and supporting long-term financial sustainability aligned with climate goals.

- Key Change: Subscribers can now withdraw a larger lump sum while reducing the mandatory annuity requirement.

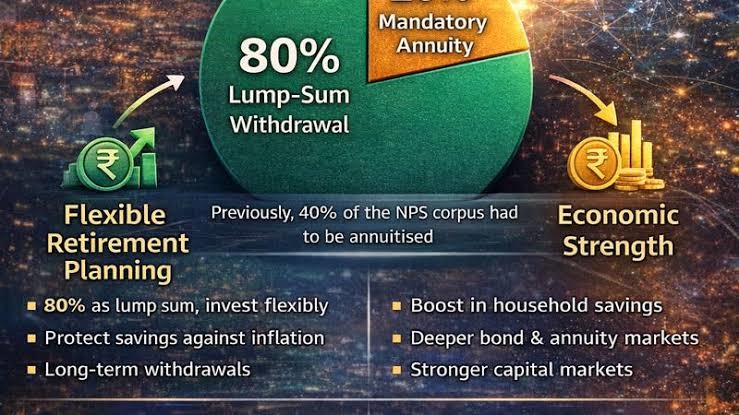

NEW NPS WITHDRAWAL RULES

- Higher Lump Sum: The mandatory annuity purchase has been reduced from 40% to 20%, allowing subscribers to withdraw up to 80% of the retirement corpus as a lump sum.

- Small Corpus Relief: Subscribers with an accumulated corpus of up to ₹8 lakh can withdraw the entire amount, while those with ₹8–12 lakh receive graded withdrawal benefits.

- Retirement Income Scheme (RIS): A new Retirement Income Scheme enables phased withdrawals while keeping the remaining corpus invested for continued market-linked returns.

- Withdrawal Options: RIS offers Systematic Lump Sum Withdrawal (SLW) with fixed periodic payouts and Systematic Unit Redemption (SUR) where payouts vary according to the Net Asset Value (NAV).

- Significance: The reforms provide greater financial flexibility, improve retirement income planning, and reduce excessive dependence on low-return annuity products.

CHALLENGES AND IMPLICATIONS

- Taxation Issue: While PFRDA permits withdrawal of 80%, the Income Tax Act currently exempts only 60%, making the additional 20% taxable until tax laws are amended.

- Longevity Risk: Greater access to retirement savings increases the responsibility on retirees to manage funds prudently throughout longer life expectancy.

- Investment Discipline: Poor financial planning or excessive withdrawals may result in depletion of retirement savings before the end of retirement.

- Comparison with Mutual Funds: RIS functions similarly to a Systematic Withdrawal Plan (SWP) but offers lower costs under NPS, although with comparatively fewer investment choices.

- Policy Importance: The reforms seek to balance liquidity, retirement security, and long-term financial sustainability while encouraging wider participation in pension savings.

NATIONAL PENSION SYSTEM (NPS)● Overview: The National Pension System (NPS) is a voluntary, defined-contribution pension scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA) to provide retirement income. ● Eligibility: It is open to all Indian citizens, including Non-Resident Indians (NRIs), generally between the ages of 18 and 70 years. ● Structure: NPS operates through Tier-I (mandatory retirement account) and Tier-II (voluntary savings account), with investments managed by licensed Pension Fund Managers (PFMs). ● Investment Pattern: Contributions are invested in a mix of equity, corporate bonds, government securities, and alternative assets, based on the subscriber’s chosen asset allocation. ● UPSC Relevance: Important under GS Paper III – Indian Economy, Financial Markets, Social Security, Pension Reforms, Financial Inclusion, and Regulatory Institutions. |