Income Tax Bill 2025: Digital Search Powers Explained

REVISIT DIGITAL SEARCH POWERS UNDER INCOME TAX BILL 2025

Syllabus:

GS-3: ● India Economy and development ● Taxation

Why in the News?

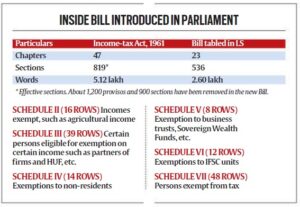

The Income-Tax Bill, 2025, introduced in Parliament by Finance Minister Nirmala Sitharaman during the monsoon session, proposes to empower tax officials with access to an individual’s “virtual digital space” during search and seizure operations. While aiming to modernize tax administration amid rising digital transactions in the digital economy, this move has raised grave concerns regarding digital privacy, surveillance, and constitutional safeguards. The bill seeks to update the income tax and direct taxes framework to address contemporary challenges in the digital era.

SHIFT FROM PHYSICAL TO DIGITAL DOMAIN

The proposal reflects a paradigm shift from physical spaces to vast and intimate digital realms, altering the foundational logic of tax enforcement and the income tax law.

- Expanded Scope: The existing income tax act targets physical premises like houses and offices, but the proposed changes include emails, cloud storage, social media, and more, encompassing a wide range of digital information and computer systems.

- Blurring Boundaries: A clear nexus between physical assets and undisclosed income is lost, as digital platforms contain diverse personal and professional data, including electronic documents and records.

- Third-Party Exposure: Social media and collaborative tools involve multiple stakeholders, risking exposure of friends, clients, and family through access to social media accounts and private communications.

- Unrestricted Wording: The phrase “any other space of similar nature” in the Income Tax Bill is open-ended, risking arbitrary interpretation and potentially extending to various computer resources and digital application platforms.

- Operational Ambiguity: Accessing encrypted platforms like WhatsApp raises concerns about technical feasibility and overreach, particularly regarding security protocols and email servers.

RISKS TO PRIVACY AND PROFESSIONAL INTEGRITY

The Income Tax Bill threatens privacy rights, particularly of professionals handling sensitive or confidential data.

- Journalistic Risk: Journalists’ devices may hold confidential sources and unpublished reports, exposing them to threats and intimidation through access to their communication devices.

- Legal Violations: Seizing devices without judicial oversight can violate Article 21, which ensures right to privacy and personal liberty, potentially infringing on data protection principles.

- SC’s Position: The Supreme Court’s 2023 interim guidelines stressed formulating protocols for digital seizures, reinforcing the gravity of intrusion and the need for a robust legal framework.

- Beyond Suspicion: Judicial interpretation of “reason to believe” mandates tangible evidence, not mere assumptions, emphasizing the importance of proper digital evidence handling.

- Massive Exposure: Devices often contain decade-long records, including financial and non-financial personal histories, risking disproportionate access to an individual’s entire digital footprint, including demat accounts and trading accounts.

LACK OF SAFEGUARDS AND ACCOUNTABILITY

The Bill lacks the necessary guardrails, making it incompatible with the principles of natural justice and due process.

- Opaque Provisions: The reasons for digital access are undisclosed, violating principles of transparency and informed consent.

- No Judicial Oversight: Absence of prior authorization or oversight by a neutral authority opens the door to arbitrary actions, potentially undermining the rule of law.

- Sweeping Powers: The provision allows bypassing access codes, indicating excessive empowerment of tax officials and raising concerns about data misuse.

- Ignored Precedents: International and domestic precedents for proportional and limited access are not incorporated, diverging from global best practices in digital banking and fintech operations.

- Risk of Abuse: Without checks, such powers may intimidate dissenting voices, affecting democratic functioning and potentially compromising fiscal integrity.

GLOBAL STANDARDS FOR DIGITAL SEARCH

Countries like Canada and the U.S. follow structured and rights-based approaches to digital surveillance.

- Canadian Model: Canada mandates a three-part test—prior authorization, neutral approval, and probable cause—under Section 8 of the Charter.

- US Due Process: The IRS’s Taxpayer Bill of Rights upholds that enforcement should be “no more intrusive than necessary.”

- Riley v. California: The U.S. Supreme Court insists on warrants for digital searches due to personal data sensitivity.

- Comparative Lag: India’s proposal lacks specificity and proportionality, falling short of international best practices in handling electronic media and digital wallets.

- Trust Deficit: Absence of global-standard safeguards can reduce public trust in tax institutions and governance mechanisms, particularly concerning cryptocurrency transactions and e-commerce operations.

VIOLATION OF PROPORTIONALITY PRINCIPLE

The Bill directly contradicts the Puttaswamy Judgment, which established privacy as a fundamental right.

- Proportionality Ignored: The Bill bypasses the four-fold test—legitimate aim, necessity, relevance, and least restrictive alternative, failing to meet the proportionality test.

- No Relevance Filter: It doesn’t distinguish between financial records and private personal content on digital devices, potentially exposing unrelated financial activities.

- Judicial Bypass: No requirement for a warrant or neutral judicial review, undermining checks and balances in the taxation system.

- Excessive Intrusion: Invasive access to an individual’s complete digital footprint goes against the doctrine of minimal interference, raising concerns about device seizure.

- Erosion of Rights: The attempt to enforce tax compliance must not erode constitutional rights and liberties, particularly in the context of emerging technologies.

RECOMMENDATIONS AND WAY FORWARD

Reform should combine efficient enforcement with constitutional safeguards, ensuring balance between state interests and civil liberties.

- Redefine Scope: Narrow the definition of ‘virtual digital space’ to only those domains relevant to financial investigation, such as cloud-based accounting systems.

- Mandate Warrants: Introduce a requirement for prior judicial authorization, similar to search warrants under criminal law for accessing computer networks.

- Establish Protocols: Frame clear guidelines on access to encrypted communications and data segregation mechanisms to protect against cyber threats.

- Protect Professionals: Special protections for journalists, lawyers, and other professionals handling confidential third-party data on peer-to-peer platforms.

- Grievance Redressal: Set up mechanisms for redressal and appeal to ensure accountability for misuse or overreach in search operations.

NEED FOR TECHNO-LEGAL BALANCE

Modernizing enforcement must not come at the cost of legal norms and democratic ethos.

- Guarded Innovation: While tax enforcement must evolve, it must stay anchored in constitutional values and due process, especially when dealing with digital information.

- Technology Ethics: Usage of digital tools should be ethical, proportionate, and auditable by independent authorities, particularly for accessing online marketplaces.

- Data Sovereignty: The rise of digital governance must coincide with citizens’ sovereignty over their own data and privacy on the worldwide web.

- Context-Specific Reforms: Any framework must account for India’s unique digital landscape, involving millions of new users across various digital application platforms.

- Democratic Principles: Governance cannot rely on blanket powers, especially in matters as sensitive as personal data stored on diverse computer resources.

CONCLUSION

The Income Tax Bill, 2025, though progressive in scope, must be legally tempered to avoid turning enforcement into surveillance. A recalibration rooted in privacy, proportionality, and purpose limitation is urgently required. Empowerment of the state must not come at the cost of citizens’ rights, especially in a democratic, digital India. The bill should be referred to a select committee of the Lok Sabha for further scrutiny and to ensure it aligns with fundamental rights and addresses cybersecurity concerns. Proper procedural safeguards and warrant requirements need to be incorporated to protect against privacy violations and unauthorized access to digital assets and virtual digital assets. The legislative reforms should strike a balance between enabling effective tax administration in the digital realm and safeguarding constitutional rights in an era of rapid digital transformation.

MAINS PRACTICE QUESTION

Critically examine the digital search and seizure powers proposed under the Income-Tax Bill, 2025. How do they align with constitutional safeguards related to privacy and proportionality? Suggest suitable reforms. (15 Marks)