India’s Middle Class 2.0: Challenges and Growth

Syllabus:

GS-2:

Important International Institutions

GS-3:

Growth & Development

Focus:

The rise of India’s middle class, driven by private sector growth, especially in IT and banking, has reshaped the employment landscape. However, structural challenges remain, particularly in manufacturing, income inequality, and informal sector jobs, which need to be addressed for inclusive growth.

Rise of Private Sector Employment

- Transformation of Employment Landscape

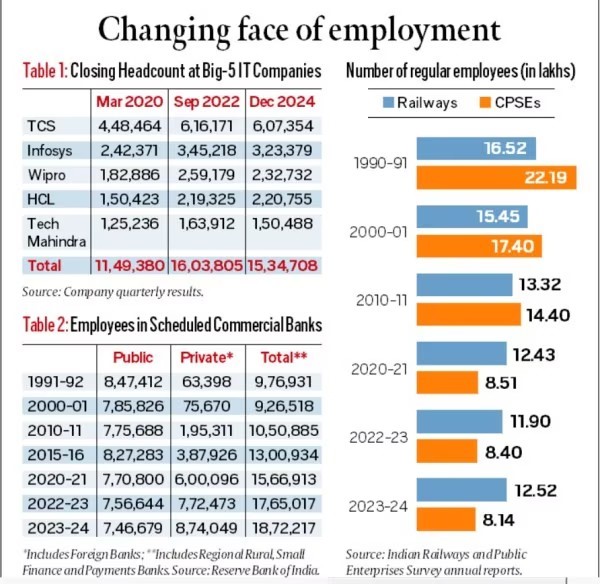

- The growth of private sector industries has shifted the traditional employment base in India. Information Technology (IT) firms like TCS, Infosys, Wipro, HCL, and Tech Mahindra now employ more people than the Indian Railways and the armed forces

- This shift has drastically changed India’s employment dynamics, contributing to the expansion of the Middle Class 2.0.

- The Expansion of IT Sector

- TCS, Infosys, and other IT giants employed over 16 lakh individuals by 2022. This marks a significant increase from 5 lakh employees in 2020.

- The COVID-19 pandemic accelerated digitalization, benefiting IT exports and creating more job opportunities, highlighting the prominence of digital services in India’s economy.

- Private Sector Growth in Banking

- Similarly, private sector banks now employ more individuals than state-owned counterparts, reflecting a significant change in the financial sector. For example, in 2023-24, HDFC Bank, ICICI Bank, and others employed over 61 lakh people, surpassing the employment figures of public sector banks like the State Bank of India (SBI).

- The shift to private banks reflects a larger trend of liberalization and globalization opening up more private sector roles.

Understanding Middle Income Trap:

- Definition: A situation where a country, having moved from low-income to middle-income status, gets “stuck” and struggles to transition to high-income status.

- World Bank Threshold: Typically occurs when a country’s per capita income reaches about 11% of US per capita income levels.

- Challenges:

- Too expensive to compete with low-wage economies in manufacturing.

- Lacks technological sophistication and innovation capabilities to compete with advanced economies.

- Traditional growth drivers lose effectiveness.

- Rising wages make labor-intensive exports less competitive.

- Struggles to develop innovation and productivity for knowledge-based growth.

- World Bank’s “3i” Approach:

- Investment in physical and human capital.

- Infusion of new global technologies.

- Fostering domestic innovation capabilities.

- Difficulty: Only 34 middle-income economies have successfully transitioned to high-income status over the last 34 years.

India’s Income Level Evolution:

- 1950s-1970s (Post-Independence Era):

- Per capita income: ₹265 in 1950-51.

- Slow growth rate (~3.5%), agriculture dominated.

- High poverty rates (~45%).

- Heavy state intervention and emphasis on public sector enterprises.

- 1980s-1990s (Pre & Early Liberalization):

- Per capita income growth accelerated to 5.6% in the 1980s.

- 1991 liberalization opened the economy.

- Rise of services sector, surpassing agriculture.

- Middle class expansion and foreign exchange reserves grew to USD 5.8 billion in 1991.

- 2000-2010 (High Growth Phase):

- High GDP growth (~8-9% annually).

- Per capita income rose from ₹16,173 in 2000-01 to ₹24,295 by 2007-08.

- Dominance of the services sector.

- Software service exports grew from $0.5 million in 1990 to $23.6 billion in 2005-06.

- 2010-2020 (Mixed Growth Phase):

- Growth rate averaged 6-7%.

- Per capita income reached ₹1,08,645 (2019-20).

- Significant middle-class expansion (400 million people).

- Rising inequality: top 1% owned 40.5% of national wealth by 2021.

- 2020-Present (Post-Covid Recovery):

- GDP reached $3.75 trillion despite Covid setbacks.

- Per capita income: ₹1,72,000 (2022-23).

- K-shaped recovery evident.

- Gig economy grew with 7.7 million workers.

- UPI digital payments processed ₹80.8 lakh crore ($964 billion) in April-July 2024, a 37% year-on-year increase.

- Unemployment at 8.1% (April 2024).

Changing Nature of Jobs in India:

- Dominance of Services Sector

- The services sector in India, including IT, finance, healthcare, retail, hospitality, and logistics, has seen substantial growth. However, this job growth has been concentrated in the formal and high-skill sectors, primarily benefiting better-educated

- Service jobs in construction, domestic work, retail, and the gig economy often pay low wages, which prevents many workers from entering the expanding Middle Class 2.0.

- This shift has exacerbated income inequality, as the demand for skilled labor increases, while unskilled jobs

- The Gig Economy’s Impact

- The gig economy is booming, with Uber employing over 10 lakh drivers, Zomato and Swiggy engaging thousands of delivery personnel. However, these jobs are largely informal, low-paying, and insecure, preventing workers from achieving upward social mobility or entering the higher echelons of the middle class.

- Job Creation in Key Sectors

- While IT, banking, and finance have created numerous formal sector jobs, sectors such as healthcare, tourism, aviation, and media have also contributed to Middle Class 2.0 However, these sectors often require specialized training or education, leaving out many potential workers.

Structural Challenges in Employment:

- Lack of Structural Transformation

- Unlike countries like China, India has not experienced significant structural transformation in its economy. The major shift from agriculture to manufacturing or modern services that India needed to undergo has not happened to the same extent.

- The agriculture sector still employs a significant portion of India’s workforce, although its share has declined from 64% in 1993-94 to 42% in 2023-24. On the other hand, manufacturing’s share of employment has stagnated at around 11%.

- The Lag in Manufacturing

- Despite India’s efforts to promote Make in India and develop its manufacturing sector, manufacturing has not seen substantial growth. The latest figures from the Periodic Labour Force Survey (PLFS) indicate that manufacturing employment has not significantly risen in proportion to India’s growing workforce.

- India’s manufacturing sector lags behind other emerging economies like China, which has seen substantial growth in industrial output and labor productivity, driving the country’s middle class expansion.

Employment in the Public and Private Sectors:

- Decline of Public Sector Employment

- Public sector employment has seen a sharp decline over the past few decades. For instance, the number of employees in the Indian Railways has fallen from 5 lakh in 1990-91 to 11.9 lakh in 2022-23.

- Employment in Central Public Sector Enterprises (CPSEs) has also decreased, from 2 lakh in 1990-91 to just over 8 lakh by 2023-24. This shift has been part of the ongoing process of liberalization and privatization in India.

- Shift from Public to Private Sector

- Post-1991 economic reforms, the organized private sector has seen a substantial increase in employment. The IT industry and private banks have been significant drivers of this shift.

- In contrast, the public sector, which used to be the largest employer in the country, now provides far fewer jobs compared to the private sector. This trend has reshaped India’s middle class, giving rise to Middle Class 2.0.

The Future Employment Challenge:

- The Need for Manufacturing Jobs

- To sustain the growth of Middle Class 2.0, India must address the jobs crisis in the manufacturing sector. While services have expanded, they cannot absorb all the labor force, particularly for individuals with lower levels of education and skills.

- The government’s focus should be on boosting industrial employment through initiatives like Make in India, improving labor skills, and promoting technology-driven manufacturing.

- Policy Focus on Education and Skills

- To ensure that Middle Class 2.0 remains sustainable, India must invest heavily in education and vocational training. This would empower more individuals to transition from low-wage, informal jobs into formal, skilled roles in high-growth sectors like IT, healthcare, and financial services.

- Addressing Income Inequality

- A key challenge will be to address the growing income disparity within the new middle class. While some sectors have seen wage growth, many others remain stagnated, especially in the informal sector.

- Government policies should aim to enhance wages, provide social security, and ensure equal opportunities for all workers to move into higher-paying sectors.

Conclusion:

India’s Middle Class 2.0 represents a major shift in the country’s employment landscape, fueled by private sector growth, particularly in IT and banking. However, challenges remain in the form of an underdeveloped manufacturing sector, a large informal labor market, and income inequality. To ensure the continued growth of a more inclusive middle class, India needs to focus on expanding manufacturing, improving education and skills, and addressing the challenges of income disparity.

Source: TH

Mains Practice Question:

Discuss the challenges faced by India’s “Middle Class 2.0” and suggest policy measures to promote inclusive economic growth. How can India address the issue of income inequality within this new middle class?